Stablecoins are one of the most useful things crypto has built.

Not the loudest. Not the weirdest.

Not the one with a cartoon animal yelling about community.

Useful.

They move like crypto, price like dollars, and settle without asking a bank branch what time it is.

That is a real upgrade. But here is the part people skip:

Faster money is not automatically safer money.

Stablecoins improve the rails. They do not delete risk. They change where the risk lives.

In traditional finance, the risk sits inside banks, payment processors, settlement windows, custody rules, chargeback systems, compliance departments, and legal wrappers.

On chain, the risk moves into issuers, reserves, wallets, blockchains, smart contracts, liquidity, redemption paths, and whatever the user signs at 1:14 a.m. because the interface looked clean.

Progress? Yes.

Magic? No.

Stablecoins are not a side quest anymore

This is no longer a niche crypto topic.

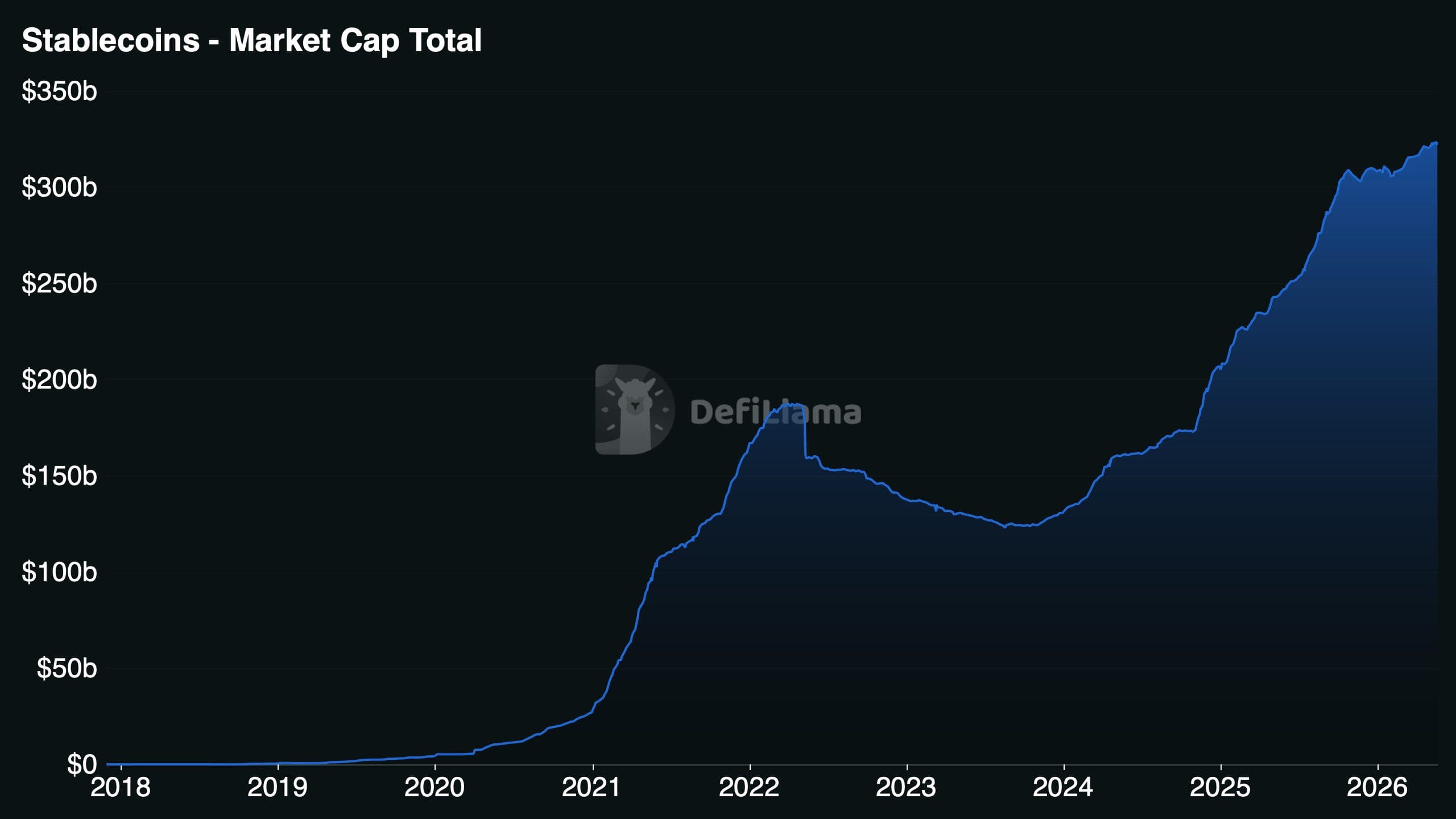

As of May 22, 2026, DeFiLlama shows total stablecoin market cap at roughly $322.1 billion. USDT is around $189.6 billion, and USDC is around $76.3 billion.

Visa’s stablecoin dashboard, using its own adjusted methodology, shows more than $272 billion in global circulating stablecoin supply and about $10.2 trillion in adjusted global transaction volume over the last 12 months.

That scale changes the conversation.

When a market is small, people ask:

“Is this real?”

When a market is over $300 billion, the better question is:

“What is this becoming, and what risk comes with it?”

Stablecoins are becoming crypto’s default dollar rail.

They are used for trading, settlement, treasury movement, DeFi collateral, payments, remittances, vaults, and idle capital management.

That does not mean every stablecoin is good. It means the category matters.

What a stablecoin actually is

A stablecoin is a blockchain token designed to track the value of another asset, usually the U.S. dollar.

Simple enough.

But it is not the same thing as holding dollars in a bank account.

A stablecoin is a bundle of several things:

a token

an issuer or protocol

reserves or collateral

redemption mechanics

market liquidity

blockchain settlement

wallet custody

regulatory exposure

That bundle can be powerful. It can also break in more than one place.

A stablecoin is not just “cash on-chain.” It is a claim, a token, and a payment rail wearing the same jacket.

That is why serious users should care about what backs it, where it trades, how it redeems, and what happens under stress.

Not because stablecoins are bad. Because money rails are never risk-free. They are just risk-designed.

Traditional finance is not dead. It is just limited

Crypto people love pretending traditional finance is a museum exhibit.

It is not.

Traditional rails still move enormous value, and they have legal structure, consumer protections, compliance processes, and decades of operational muscle.

ACH is a good example.

Nacha says the ACH Network reaches all U.S. bank and credit union accounts, processes payments 23¼ hours every banking day, and settles payments four times every banking day. In 2025, ACH processed 35.2 billion payments worth $93 trillion.

That is not dead infrastructure.

That is very alive infrastructure with a calendar problem.

ACH still settles during banking-system windows. Nacha notes that ACH payments are not currently settled on weekends and federal holidays.

FedNow is another example. The Federal Reserve says FedNow lets participating banks and credit unions send and receive transactions within seconds, 24 hours a day, seven days a week.

So the honest version is not:

“Banks are useless. Crypto fixes everything.”

The honest version is:

Traditional rails are improving. Stablecoins still matter because they are natively digital, global, programmable, and blockchain-connected.

That is the difference.

Stablecoins are not competing against a frozen version of banking from 1979.

They are competing against improving financial rails that still have limits.

What blockchain improves

Stablecoins make money behave more like the internet.

That sounds cliché because crypto people have abused the phrase to death.

But the point is real.

Stablecoins improve several things at once:

Improvement & What it means

24/7 movement: Value can move outside banking hours

Global access: The same token standard can move across borders and chains

Programmability: Money can interact with smart contracts

Composability: Stablecoins plug into wallets, exchanges, DeFi, vaults, and payment apps

Transparency: Supply, flows, and on-chain activity can be monitored more openly

Faster crypto funding: Users can move between cash-like balances and crypto strategies with less friction

That last point matters.

Stablecoins are not only payment assets. They are also the funding layer for on-chain finance.

A user can hold USDC, move it to a wallet, swap, lend, deposit into a vault, withdraw, bridge, or rebalance without waiting for a bank wire desk to have its morning coffee.

On Base specifically, DeFiLlama shows about $4.73 billion in stablecoin market cap, with USDC dominance around 89.8%.

That matters because low-friction chains make stablecoin workflows easier.

Good.

They also make bad decisions easier.

Less friction is not the same as more wisdom.

Speed is not a risk model.

This is the direction behind HodlyCrypto: faster stablecoin rails are useful, but users still need clearer context before moving money on-chain. Better UX should not require blind trust.

What stablecoins do not improve

Stablecoins do not remove financial risk. They move it. The risk stack changes.

Issuer risk

Who issued the stablecoin? Can they redeem it? Do they have the reserves they say they have?

Reserve risk

What backs the token? Cash? Treasuries? Repo? Bank deposits? Other assets?

The difference matters when markets are calm. It matters more when they are not.

Depeg risk

A stablecoin is supposed to trade around $1.

“Supposed to” is not the same as “must.”

Stress can break assumptions.

Banking risk

Even stablecoins live partly inside traditional finance. Issuers need banks, custodians, treasury markets, payment systems, and redemption partners. The old system is still underneath the new rail. Fun little plot twist.

Smart contract risk

The token, vault, bridge, or DeFi app may depend on code.

Code can be audited. Code can also break.

Wallet risk

Self-custody gives users control. It also gives users responsibility.

Private keys do not care that you were tired.

Liquidity risk

A stablecoin can look fine until liquidity gets thin.

A token can look liquid until everyone wants the same exit.

Regulatory risk

Rules are moving.

In the U.S., Treasury proposed rules in April 2026 to implement parts of the GENIUS Act, including anti-money-laundering and sanctions compliance requirements for permitted payment stablecoin issuers.

That does not mean stablecoins are doomed.

It means the market is maturing.

And mature markets come with rules, constraints, and tradeoffs.

The Federal Reserve made the broader point clearly in an April 2026 note: stablecoins grew sharply in 2025, but their expanding role can create new financial stability vulnerabilities through more complex intermediation chains, vertical integration, and retail adoption.

Translation:

Stablecoins reduce some friction. They introduce a different risk stack.

History lesson: USDC and Silicon Valley Bank

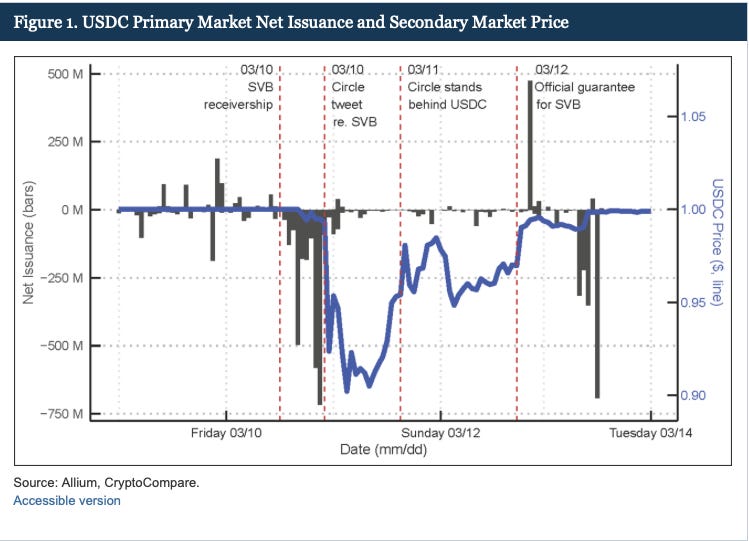

USDC is generally considered one of the higher-quality stablecoins in crypto. But in March 2023, it still temporarily lost its peg after Circle had $3.3 billion deposited with Silicon Valley Bank, around 8% of total reserves at the time. The Federal Reserve later described how Circle’s inability to access those reserves sparked redemption pressure and secondary-market selling pressure on USDC.

Chainalysis also wrote that Circle’s $3.3 billion exposure to SVB prompted USDC to lose its peg over that weekend, before the peg was regained.

USDC recovered. That matters. But the episode still taught a useful lesson:

Stablecoin risk is not only on-chain. Sometimes the weak point is the traditional financial system underneath it.

Banks matter. Reserves matter. Redemption windows matter. Market confidence matters.

Stablecoin users should not ignore the boring parts. The boring parts are usually where the real risk hides.

How to stay ahead

Stablecoins are going to keep growing. Traditional finance is going to keep adapting. Blockchains are going to keep improving the rails. Regulators are going to keep writing rules.

So the useful question is not:

“Are stablecoins good or bad?”

The useful question is:

“What improved, and what risk moved?”

Before using a stablecoin, ask:

1. Who issued it?

Is it issued by a company, a protocol, or something more experimental?

2. What backs it?

Cash, Treasuries, bank deposits, crypto collateral, algorithms, or vibes wearing a blazer?

3. Can it be redeemed?

A stablecoin is stronger when redemption is clear and reliable.

4. Has it held its peg under stress?

Normal markets do not test much.

Stress does.

5. What chain is it on?

The asset matters. The rail matters too.

6. How liquid is it?

A token can look stable until the exit gets crowded.

7. What wallet risk am I taking?

Self-custody is powerful.

It is also unforgiving.

This is not about avoiding every risk.

Crypto has risk.

Stablecoins have risk.

Self-custody has risk.

The goal is to know which risk moved before you move the money.

The takeaway

Stablecoins are an upgrade.

They make money faster, more programmable, more global, and more useful inside crypto.

But they are not magic dollars.

They are not risk-free cash.

They are not automatically safer because they live on a blockchain.

Traditional finance has slow rails and heavy intermediaries.

Blockchain has fast rails and sharper user responsibility.

Both have tradeoffs.

The smart move is not to pick a team and stop thinking.

The smart move is to understand what improved and what risk moved.

Stablecoins fixed part of the rail problem.

They did not delete issuer risk.

They did not delete reserve risk.

They did not delete depeg risk.

They did not delete smart contract risk.

They did not delete wallet risk.

They did not delete liquidity risk.

That is the direction behind HodlyCrypto: calmer accumulation, clearer risk, and user-controlled execution.

Not “move faster and hope.”

More like:

What am I using, what risk moved, and what could break under stress?

That question will not make stablecoin risk disappear.

It will make the user harder to fool.

And in crypto, that is already a decent edge.

Stablecoins are the rail upgrade.

Yield is the next layer.

Holding USDC is one decision. Putting that USDC into a vault for APY is another. That second decision needs its own framework: who pays the yield, who controls the vault, how liquid the exit is, and what risk the APY is paying you to take.

That is Part 2.

Not financial advice. Stablecoins can depeg. On-chain assets carry smart contract, liquidity, wallet, issuer, reserve, regulatory, and market risk.