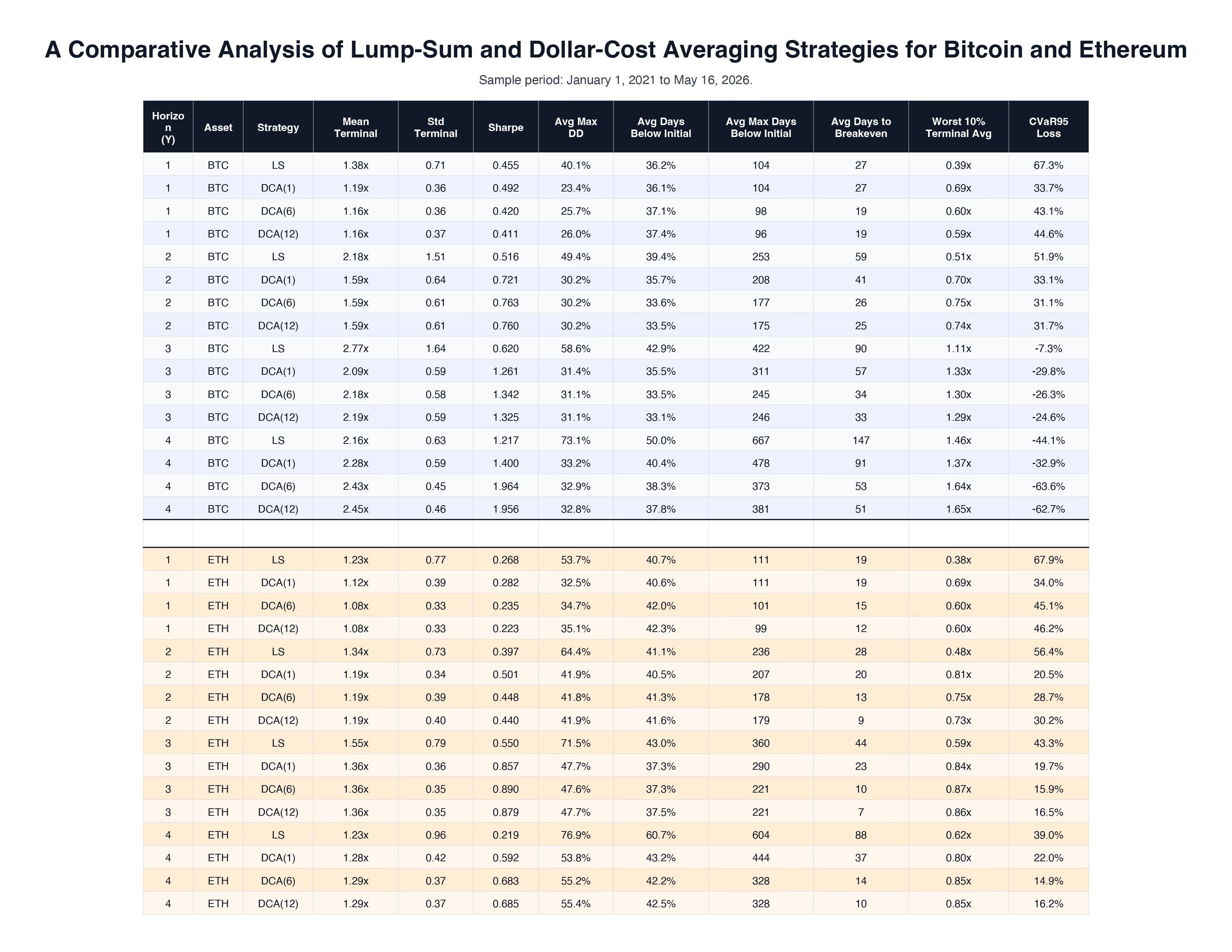

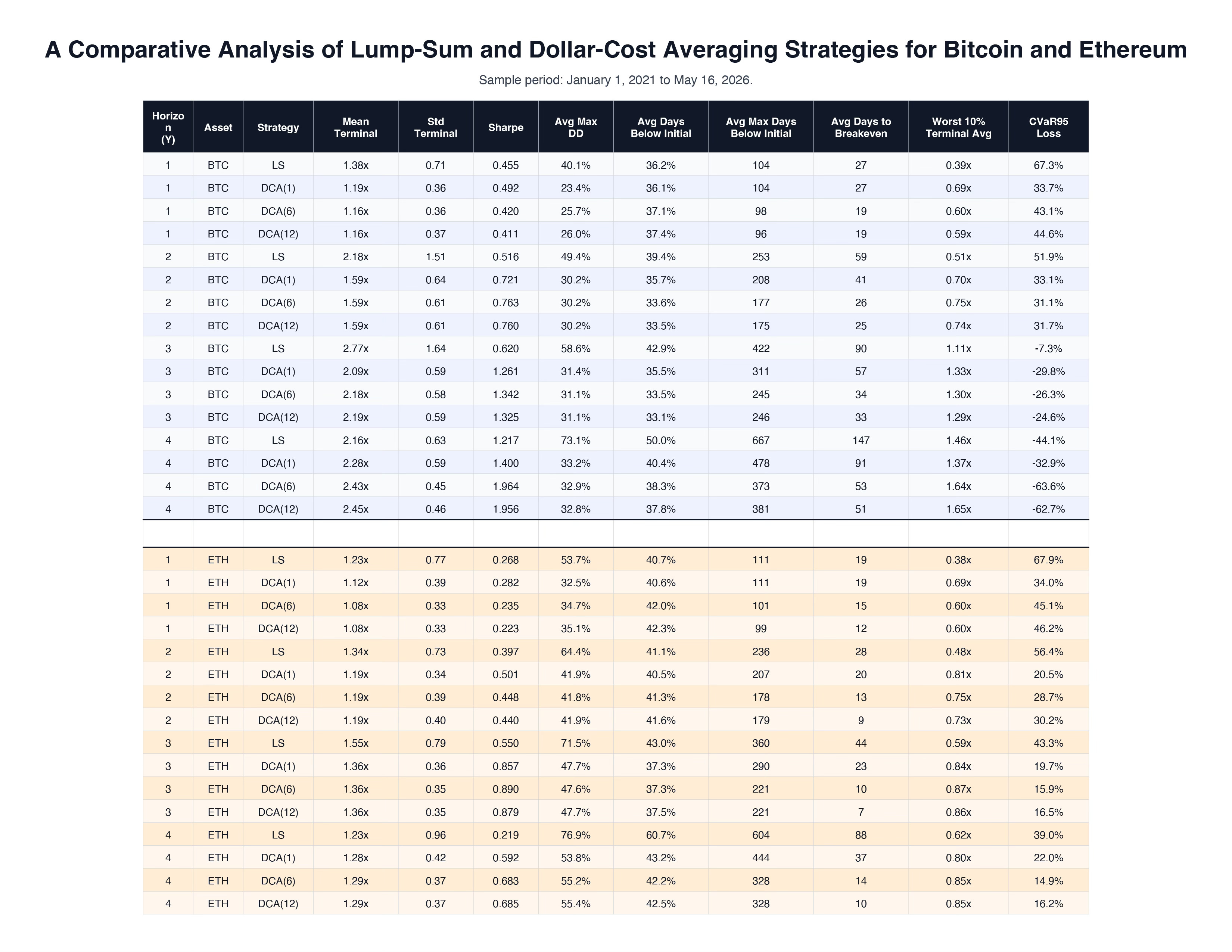

Here the test result:

Strategies tested:

LS = invest all capital immediately

DCA(1) = split investment over yearly intervals

DCA(6) = split investment over 6 periods per year

DCA(12) = monthly DCA

How to read the table:

Mean Terminal = average final portfolio value. Higher is better.

Std Terminal = how spread out the final outcomes are. Higher means more uncertainty around the result.

Sharpe = return per unit of volatility. Higher is better.

Avg Max DD = average maximum drawdown. Lower is better.

Avg Days Below Initial = average percent of time the strategy stayed below the starting capital. Lower is better.

Avg Max Days Below Initial = average longest stretch spent below starting capital. Lower is better.

Avg Days to Breakeven = average time needed to recover back to starting capital after falling below it. Lower is better.

Worst 10% Terminal Avg = average final result from the worst 10% of starting periods. Higher is better.

CVaR95 Loss = average loss in the worst 5% of outcomes. Lower is better.

Key takeaway:

LS wins big on return for both BTC and ETH

LS generally fails on remaining metrics, except for Avg Days Below Initial

More frequent DCA is not always better.

Question:

“Do we need an accumulation strategy that improves long-run survivability without giving up too much return?”

Deeper analysis coming…