In traditional finance, cash sitting in a bank can earn interest. DeFi yield brings the same basic idea on-chain, letting you put crypto assets to work inside decentralized protocols to generate returns.

Regarding the ongoing debate over which yield product is the best, here’s my answer: Every strategy has an engine that generates the return, and every engine has parts that can fail. Besides the holy-grail APY %, you should choose yield product based on this question: “What can you tolerate?”

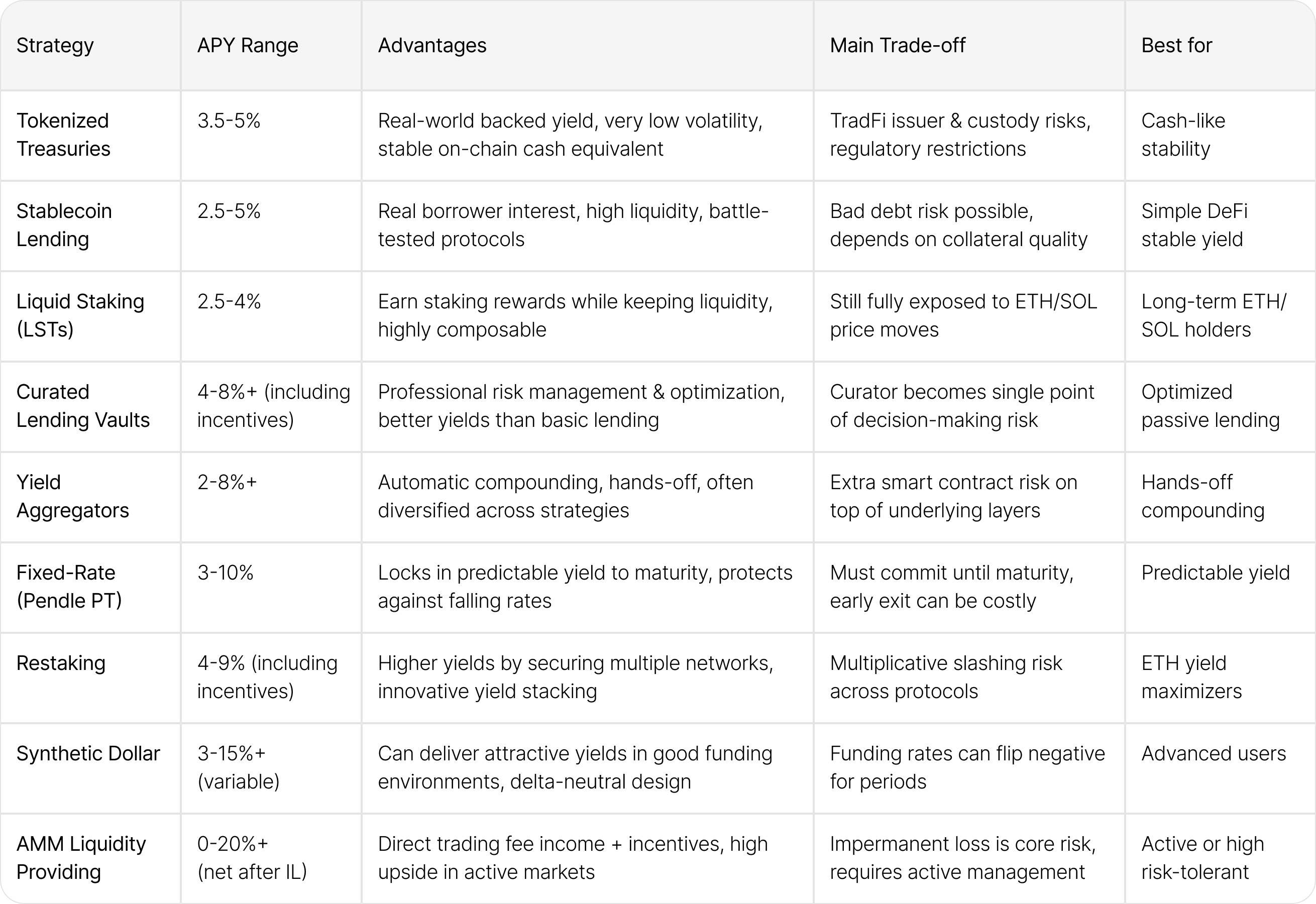

1. Tokenized Treasuries (BlackRock BUIDL, Ondo USDY/OUSG)

These are on-chain tokens backed by real U.S. Treasury bills and short-duration government debt. The yield comes directly from traditional fixed-income returns, not from crypto activity.

Typical APY range: 3.5–5.5%

What’s worth understanding

You’re swapping crypto-native risks for TradFi ones. The main exposures are issuer/custody risk and redemption terms. Liquidity is generally good, but some products have minimums or processing delays. This is the closest thing in DeFi to a cash-like yield with minimal price volatility.

Key downside

Restricted for US-citizen or available only for institution. Issuer default (extremely rare for T-bills), custody issues, or sudden redemption restrictions during market stress.

Who it suits

People who want yield on stable value with the lowest possible crypto volatility.

2. Stablecoin Lending (Aave, Compound, Spark)

You supply stablecoins to a lending market and earn the interest that borrowers pay.

Typical APY range: 3–7% on major stablecoins (higher on optimized/curated pools)

What’s worth understanding

This is one of the cleanest DeFi yield models. The yield is real borrower interest, not token emissions. However, “overcollateralized” does not mean risk-free. Bad debt can still occur if collateral drops sharply or oracles fail. Note: Lending volatile assets (ETH, BTC, etc.) adds major price risk and higher liquidation chance.

Key downside

Oracle manipulation, sudden collateral devaluation leading to undercollateralized loans, or liquidity crunches during black swan events.

Who it suits

Investors comfortable with core DeFi mechanics who want straightforward stablecoin yield.

3. Liquid Staking Tokens – LSTs (Lido stETH, Rocket Pool rETH, JitoSOL)

You stake ETH or SOL and receive a liquid token that continues earning staking rewards while remaining tradable.

Typical APY range: 2.5–4% (base staking yield; can be higher with additional incentives)

What’s worth understanding

This is not “safe yield.” You remain fully exposed to ETH or SOL price movements, plus you now carry validator concentration risk and the possibility of the LST trading at a discount to the underlying asset during stress.

Key downside

A major slashing event, validator concentration issues (especially on Lido), or temporary depeg during market panic.

Who it suits

Long-term ETH or SOL holders who want to earn yield on assets they already plan to keep.

4. Curated Lending Vaults (Morpho Vaults and similar curator-managed pools)

Professional curators or algorithms allocate your capital across multiple lending markets to optimize yield while managing risk parameters.

Typical APY range: 4–8%+ (depending on curator and market conditions)

What’s worth understanding

The curator becomes the new decision-making layer. They choose which markets to use and how much risk to take. This can improve returns, but it also concentrates risk into one team’s judgment and allocation decisions.

Key downside

Curator misallocation, sudden changes in market parameters, or the underlying lending markets experiencing bad debt.

Who it suits

People who want better-than-basic lending yields without manually managing every market themselves.

5. Yield Aggregators & Auto-Compounding Vaults (Yearn, Beefy)

These are wrappers that automatically compound returns from underlying strategies (lending, liquidity providing, staking, etc.).

Typical APY range: 3–8% (varies widely depending on what the vault is farming)

What’s worth understanding

You’re adding an extra smart contract layer on top of whatever strategy is running underneath. The vault reduces your daily work, but you now trust both the vault code and the underlying strategy’s performance and migration decisions.

Key downside

Strategy drift (the vault starts doing something different than expected) or an exploit in the vault itself.

Who it suits

Users who want truly hands-off compounding and accept the extra layer of trust.

6. Fixed-Rate Yield Tokenization (Pendle PT positions)

You can lock in a fixed yield by buying Principal Tokens (PT) that mature at a set date.

Typical APY range (fixed PT): 4–10% depending on the underlying asset and time to maturity

What’s worth understanding

Holding PT to maturity gives you a more predictable fixed return. This is very different from buying the Yield Token (YT), which is essentially a leveraged bet on future yield movements. PT is closer to a bond; YT is closer to a derivative trade.

Key downside

The underlying yield source underperforms before maturity, or liquidity dries up if you need to exit early.

Who it suits

Investors who want certainty on yield and are comfortable holding until maturity.

7. Restaking & Liquid Restaking (EigenLayer, ether.fi, Renzo)

You take already-staked ETH (or LSTs) and reuse it to secure additional networks and services for extra rewards.

Typical APY range: 4–9% total (base staking + restaking rewards)

What’s worth understanding

Besides earning extra yield, you’re taking on slashing risk from multiple networks at once. If several of the services you’re securing get slashed simultaneously, losses can compound quickly. Liquid Restaking Tokens (LRTs) add another potential depeg layer.

Key downside

Coordinated slashing events across multiple AVSs or LRT depegging during market stress.

Who it suits

ETH holders who understand the added layers and want to maximize yield on their staked position.

8. Synthetic Dollar Yield (Ethena USDe / sUSDe)

This strategy uses collateral and short perpetual futures positions to capture funding rates and basis.

Typical APY range: Highly variable, historically 5–15%+ in favorable funding environments, but can drop significantly or turn negative for periods

What’s worth understanding

This is packaged financial engineering. The yield depends on perpetual futures funding rates staying positive. When funding flips negative for extended periods, the yield can disappear or reverse.

Key downside

Prolonged negative funding rates, hedge failure, or stress events that cause redemption pressure and depeg.

Who it suits

Advanced users who understand basis trading and funding mechanics.

9. AMM Liquidity Providing (Uniswap, Curve, Balancer)

You provide token pairs to a decentralized exchange and earn trading fees (plus any incentives).

Typical APY range: Highly variable, often 5–20%+ including incentives, but net returns after impermanent loss can be much lower

What’s worth understanding

This is market-making, not passive income. You get paid to take the risk that the two assets in your pool move apart (impermanent loss). Stablecoin pairs have lower IL but still carry stablecoin and protocol risk. Volatile pairs pay more but can lose significantly on price divergence.

Key downside

Heavy impermanent loss in a trending market or reward token incentives collapsing.

Who it suits

Users who actively manage ranges or understand they are providing a service and accepting directional risk.

TL;DR: Here’s the table comparing the 9 DeFi yield products: